Bookkeeping

7 3: Methods Under a Periodic Inventory System Business LibreTexts

FIFO encourages the rotation of stock, which can lead to better inventory quality overall. Customers receive products that are fresher or more current, which can enhance customer satisfaction and reduce the need for markdowns and waste. Thus, the above example of FIFO inventory method gives a clear idea about the valuation process. Jami Gong is a Chartered Professional Account and Financial System Consultant. She holds a Masters Degree in Professional Accounting from the University of New South Wales.

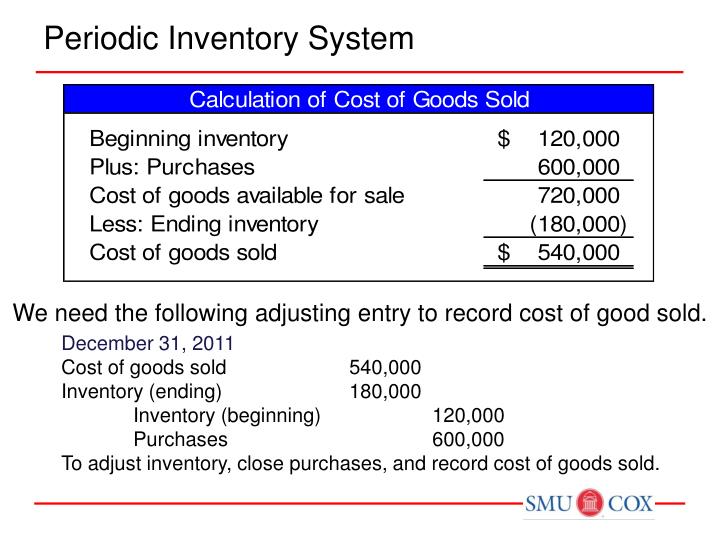

Step 3: Calculate COGS

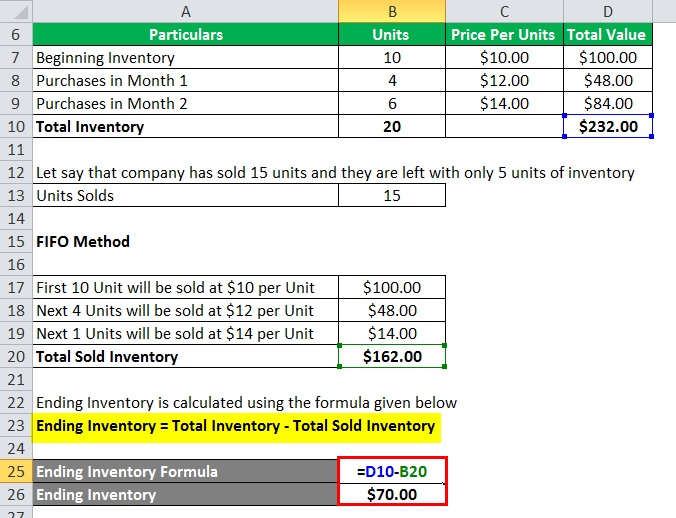

Therefore, the value of ending inventory is $92 (23 units x $4), which is the same amount we calculated using the perpetual method. Let’s say you’ve sold 15 items, and you have 10 new items in stock and 10 older items. You would multiply the first 10 by the cost of your newest goods, and the remaining 5 by the cost of your older items to calculate your Cost of Goods at what income does a minor have to file an income tax return Sold using LIFO. In times of rising prices, LIFO results in higher COGS due to the use of newer, more expensive inventory, which can lower taxable income and thus, tax liabilities. Like FIFO, LIFO (Last-In, First-Out) offers a proven valuation approach. Recent surveys reveal that approximately 55% of companies were using FIFO as their primary inventory method.

How To Calculate FIFO

- The COGS for each of the 60 items is $10/unit under the FIFO method because the first goods purchased are the first goods sold.

- Last-in, first-out values inventory on the assumption that the goods purchased last are sold first at their original cost.

- The use of FIFO method is very common to compute cost of goods sold and the ending balance of inventory under both perpetual and periodic inventory systems.

- This will ensure that your balance sheet will always be up to date with the current cost of your inventory, and your profit and loss (P&L) statement will reflect the most recent COGS and profit numbers.

- In the first example, we worked out the value of ending inventory using the FIFO perpetual system at $92.

To keep track of the movement and usage of inventory within your warehouses, implement robust inventory tracking and management processes. To minimize errors and improve overall inventory accuracy, use tools like barcode scanning and RFID tagging for accurate inventory identification and tracking. FIFO is an inventory valuation method that stands for First In, First Out, where goods acquired or produced first are assumed to be sold first.

FIFO Inventory Method Explained

The remaining inventory assets are matched to assets that were most recently purchased or produced. Businesses in industries with rising costs or prices typically use the LIFO method. This includes companies dealing with commodities, such as oil and gas firms, or those with inventory that doesn’t deteriorate, like metal or chemical producers.

Consider Real Inventory Flow

Additionally, LIFO’s reception varies globally, with some accounting standards discouraging its use, thereby limiting its applicability for international businesses. FIFO can be useful during periods of inflation when higher profits may positively affect investor perception. On the other hand, LIFO shows reduced profitability, which can provide tax advantages, in particular short-term tax relief. FIFO may help contribute to higher ending inventory balances on the balance sheet, but LIFO does the opposite. Instead of increasing inventory balances, the ending value is lower, leading to lower net income. Whereas FIFO assumes that the oldest items added to inventory are the first sold, LIFO assumes that the most recently acquired inventory is sold first.

What about LIFO?

By reflecting lower inventory costs in COGS, FIFO can result in higher profits, improved financial statements, and potentially reduced tax liabilities. Determining which stock management method best suits your business depends on several factors. To determine if FIFO is the right choice for you, assess your inventory characteristics, understand customer demands and industry standards, and review your operational requirements and goals. Consider factors such as product shelf life, inventory turnover rates, and storage capacity. Conducting a cost-benefit analysis and comparing FIFO with alternative inventory systems can also help determine which method is best for your specific needs.

It may also understate profits, which can make the business less appealing to potential investors. The First In, First Out FIFO method is a standard accounting practice that assumes that assets are sold in the same order they’re bought. All companies are required to use the FIFO method to account for inventory in some jurisdictions but FIFO is a popular standard due to its ease and transparency even where it isn’t mandated. The FIFO method can result in higher income taxes for a company because there’s a wider gap between costs and revenue.

FIFO impacts financial statements by typically reporting higher profits during inflation. It results in lower cost of goods sold and higher ending inventory values on the balance sheet. This method often leads to more current inventory valuation and can affect key financial ratios used by investors and analysts. While FIFO is generally straightforward, it can be more complex to implement than LIFO (Last-In, First-Out) in certain situations.

Not only does FIFO prevent materials from going unused or degrading, it also reduces waste and losses—not to mention storage costs. Optovue, a global manufacturer of ophthalmic imaging equipment, uses mobile software to keep FIFO rules in check while also simplifying traceability compliance. With the assistance of technology, the company operates with near-perfect inventory accuracy. The FIFO method inventory valuation is commonly used under both International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP). Connect with our sales team to learn more about our commitment to quality, service, and tech-forward fulfillment. Since inventory is an asset, it’s important to keep insight into your actual inventory values.

The cost of goods sold for 40 of the items is $10 and the entire first order of 100 units has been fully sold. The other 10 units that are sold have a cost of $15 each and the remaining 90 units in inventory are valued at $15 each or the most recent price paid. Typical economic situations involve inflationary markets and rising prices. The oldest costs will theoretically be priced lower than the most recent inventory purchased at current inflated prices in this situation if FIFO assigns the oldest costs to the cost of goods sold. FIFO operates on the principle that older stock exits first, while LIFO assumes newer items are sold before older ones.